The Managed Event

A short read ahead of Friday's listing: SpaceX set its own number, locked its own float, and manufactured its own buyer. Behind it, a frozen exit market.

M Nadal & Co Strategic Advisory | June 9, 2026

SpaceX prices Thursday after the close at a fixed $135 a share and opens Friday on the Nasdaq. There is no price range, so there is no above-or-below-range signal. The only verdict is how SPCX trades on day one.

Hyperliquid’s pre-IPO proxy launched May 18. It spiked to $230 on a chaotic first day, settled near $205, and has trended steadily lower to $155 this morning. The first-day spike was thin and means little. The slide since is telling though: down roughly a quarter into the listing. The proxy is noisy, retail, and thin, but it is the only live price discovery on a company that skipped the bookbuild. Read it with care.

The last major pre-IPO on Hyperliquid was Cerebras. The pre-IPO contract, the perp, peaked near $323. The stock opened at $350, about 8% higher. The proxy underpriced the open. If SpaceX follows that pattern, the fixed $135 clears comfortably on Friday, then gives much of it back. The open is not the story. What happens after is.

The valuation does not rest on profitability. SpaceX reported a $4.9 billion net loss in 2025, with another $4.3 billion loss in Q1 2026. Starlink carries the profitable economics. The consolidated company does not. At the $1.75 trillion target this is a real revenue company losing money fast, priced at more than 90 times trailing revenue.

The valuation rests on a forced-buyer story that is more conditional than the price implies.

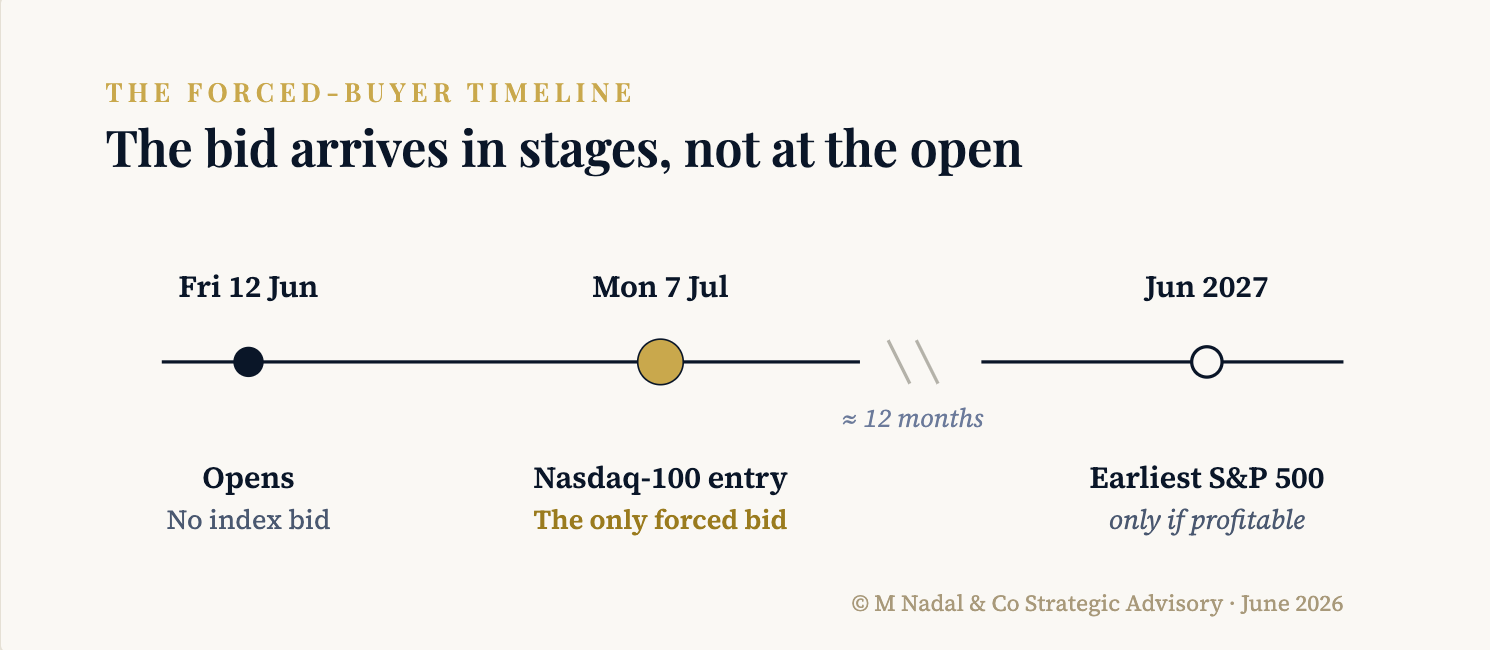

Nasdaq changed its rules effective May 1. A top-40 company can enter the Nasdaq-100 after 15 trading days, around July 7, with the float minimum waived. That is the near-term mechanical bid. S&P Dow Jones held the line. On June 4 it closed a consultation on megacap IPO eligibility and kept its rules unchanged: twelve months seasoning, profitability, and float requirements. SpaceX cannot enter the S&P 500 before June 2027, and not then unless it turns profitable. The trillions that track the S&P are not buyers until eligibility is met. The Nasdaq-100 bid is the only forced bid, and it arrives in July, not at the open.

Two constraints sit underneath. The float is thin by design, and Musk, holding over 82% voting control, is locked for 366 days. The supply that normally pressures a new listing is held back, and the index weighting that drives forced buying stays capped until the float grows.

Read these together and it is one structure. The fixed price removes the book. The float is too thin to find a level. Insiders are locked. No supply to clear. The July bid manufactures the buyer. Each removes a moment where the market would normally price the deal. The offering clears without a real demand test. That changes how to read Friday. A strong open is not the demand signal the market will treat it as. It is the structure working as designed. What it cannot fake is the grey market, which is falling, the July bid, which is finite, and the listings behind this one, which either follow or they do not.

One bid this does not name. A retail base buys Musk regardless of the losses, the float, or the multiple. It lifts the open and then exhausts. It makes Friday green. It does not reopen anything.

The larger read is about exits. The 2026 IPO revival was supposed to thaw a frozen private-market complex. Venture and growth funds holding SpaceX, OpenAI, Anthropic and the rest of the late-stage book have not returned capital to investors in years.

Those same investors are over-allocated across the whole illiquid stack, equity and credit alike, and a closed exit market freezes distributions everywhere at once.

A strong SpaceX debut keeps the window open. A weak one does not shut it alone, but it removes the proof of concept the next listings need, and the pipeline slows.

The pressure that pushed evergreen funds to gate redemptions at 5% of NAV does not ease while the exit door stays narrow.

Three branches.

Opens strong and holds (25%). Thin float and retail conviction amplify the move, the July 7 Nasdaq bid confirms it, the window reopens, distributions resume. The forced-buyer story works.

Opens above $135 then fades (55%). The retail bid fills and exhausts, the July buyer is mechanical and finite, the S&P trillions stay on the sidelines. Inflows trickle rather than resume.

Opens at or below $135 (20%). The largest US listing on record struggles despite the thinnest possible float. The proof of concept fails, the pipeline stalls, the exit window stays shut, gating pressure builds into Q3.

Falsification: The thesis is wrong if OpenAI or Anthropic prices a listing within 90 days of June 12 at or above its last private mark. The window will have reopened. It is also wrong if SPCX holds above $135 through August, past the point where the July 7 Nasdaq bid is absorbed. The demand will have been real, not mechanical.

The proxy says the open clears. The structure is designed so it does. What the structure cannot produce is the next listing. Friday is the managed event. July, and the pipeline behind it, is the test.

The deeper question, who gets to set a price at all, runs through the Oracle series. Part 2, on the architecture behind it, lands for paid subscribers this week.

If this landed, pass it on.

Disclaimer: Scenario analysis only. Not investment advice. The author holds positions in instruments discussed in Chaos & Order. Chaos & Order is not authorised or regulated by the FCA. Directed at investment professionals under Articles 19 and 49 of the FSMA 2000 (Financial Promotion) Order 2005.

© M Nadal & Co Strategic Advisory · June 2026 · chaosandorderinsight.substack.com

The price discovery question cuts deeper than the float mechanics. The contracts that don't run through the listing - the Google compute deal, the DoD relationships, the Starlink government agreements - those were priced before June 12 and don't reprice on Friday. The managed event sets the equity price. The infrastructure layer was already set. Those are two different markets operating simultaneously.