4.999%

The Private Credit Gate: What the Numbers Beneath the Marks Actually Say

STRATEGIC ADVISORY BRIEF

M Nadal & Co Strategic Advisory | April 2026

This brief uses three levels of analysis throughout.

Verified: events and data confirmed at time of publication.

Inferred: analytical conclusions from established patterns and documented relationships.

Scenario: forward-looking assessments of what follows if the inferred relationships hold. These are not predictions. They are the logical consequence of the structural dynamics mapped below.

The Hook

The same banks that structured and distributed private credit are now selling you the CDS hedge against it.

The banks now distributing a CDS index that hedges exposure to Apollo, Ares, and Blackstone (JPMorgan, Barclays, Morgan Stanley, Citigroup) are the same institutions that spent a decade underwriting, syndicating, and distributing the leveraged loans that private credit funds bought.

The CDX Financials Index launched April 10. Blue Owl was excluded from the index at inception: it was already trading at spreads too wide to include at launch. Sources: Financial Times, 17 April 2026; S&P Global CDX Financials Index launch note, February 2026.

When the people who built the product start selling insurance against it, the appraisal has already happened. You just haven’t seen the report yet.

This brief is the report.

The Signal

On April 6, 2026, Goldman Sachs filed a document with the SEC that was, in its own way, one of the most revealing filings in private credit history.

Goldman Sachs Private Credit Corp, a $15.7 billion non-traded BDC, reported Q1 2026 redemption requests of exactly 4.999% of outstanding shares. A rounding error from the industry-wide 5% quarterly cap that, once crossed, allows a fund to refuse additional redemption requests and trap investor capital for multiple consecutive quarters. Source: Goldman Sachs Private Credit Corp SEC filing and shareholder letter, April 6 2026, confirmed by Bloomberg and FA-Mag.

“We are the only non-traded BDC in the peer group whose repurchase requests came in below the standard 5% quarterly cap,” the fund wrote in its shareholder letter.

That sentence is a confession on behalf of the industry. Every single one of Goldman’s named peers crossed the gate.

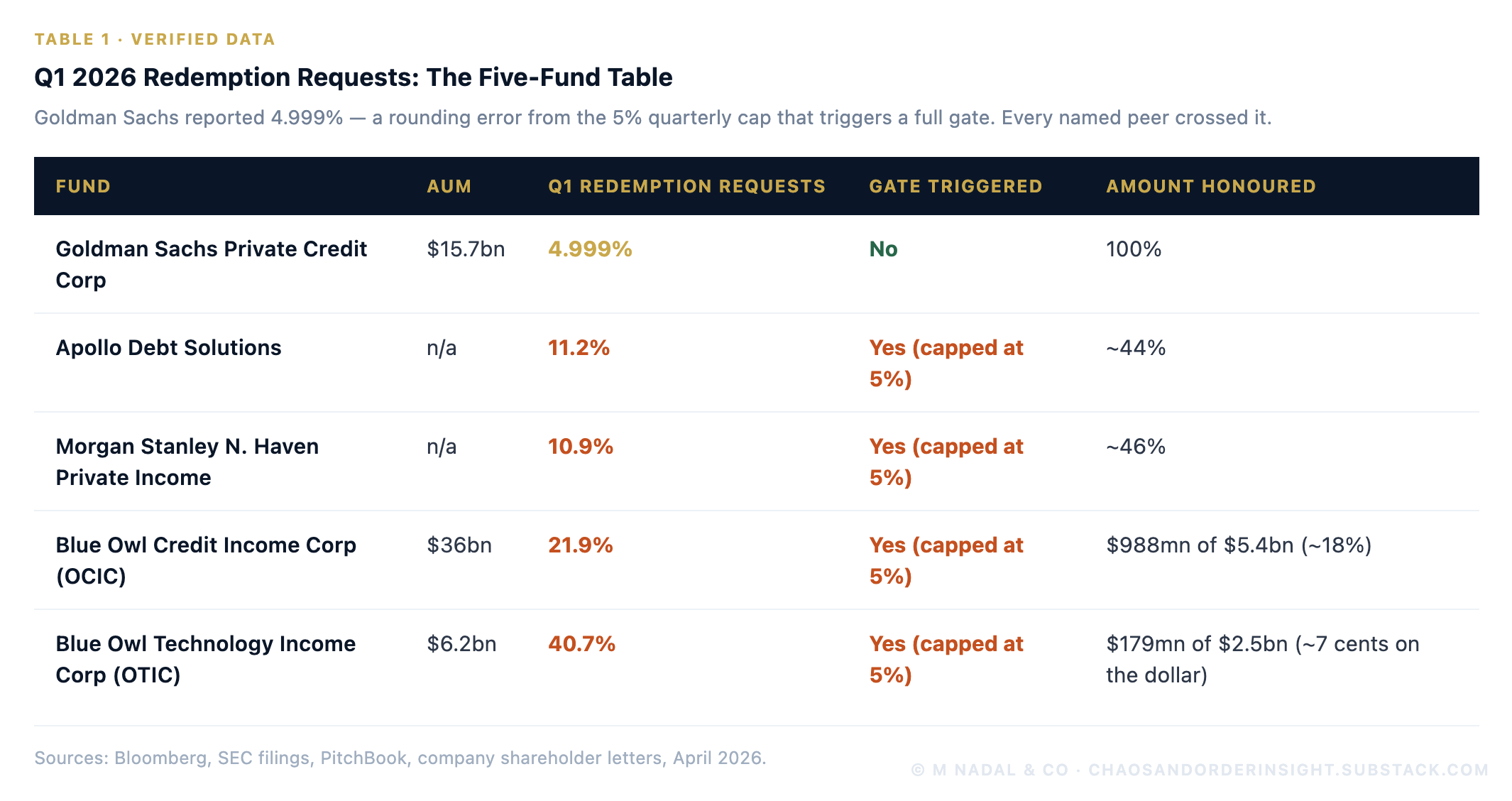

Part I: The Gate — Verified Data

Q1 2026 Redemption Requests: The Five-Fund Table

At Blue Owl OTIC, investors requesting redemption in Q1 2026 received approximately 7 cents on the dollar: $179mn honoured against $2.5bn in requests, per company earnings communications, April 2026. The fund described this outcome as operating within normal parameters.

The gate mechanism worked exactly as designed. That is the problem, not the solution.

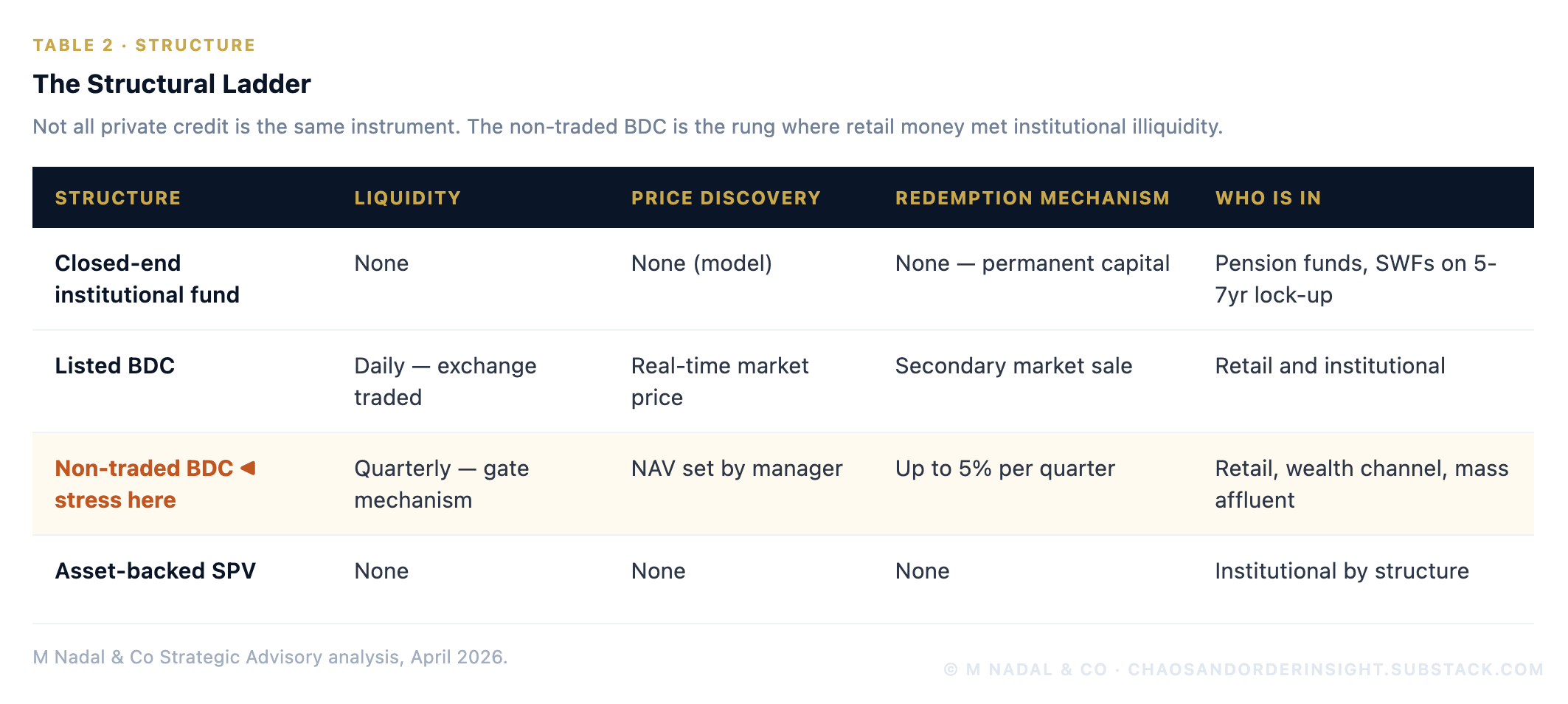

The Structural Ladder

Not all private credit is the same instrument. The distinction matters for understanding where the stress lives and where it travels next.

The non-traded BDC is the rung where retail money met institutional illiquidity. The structure was created by alternative asset managers chasing AUM growth in the retail wealth channel: more AUM, more management fees, higher stock price. The incentive was to grow and distribute. Not to ensure investors understood what they were buying.

“Not everybody has marketed their product as clearly as — certainly we would like to see — with the clarity that this is really not a liquid product. It’s not semi-liquid. It’s really illiquid. Those retail investors, I think, have the perception of more liquidity than is the reality.”

John Waldron, President and COO of Goldman Sachs, Semafor World Economy, Washington DC, 15 April 2026

Goldman’s own President. On record. About his own industry.

The five-fund table above and the structural ladder are available to all subscribers. Parts II through VII: the valuation fiction, the shadow default mechanics, the why now argument, the scenario analysis with probability weights, the earnings watch table, and the falsification conditions, are for paid subscribers.